For many prospective homeowners, one of the most pressing financial questions is: how much of your income should go to mortgage? Determining this figure is crucial to maintain a balanced budget, protect your savings, and ensure long-term financial stability. Your mortgage is typically the largest monthly expense, and allocating too much of your income toward it can strain your lifestyle, while allocating too little could limit your home-buying potential.

In this comprehensive guide, we’ll explore how much of your income should go to mortgage, analyze financial guidelines, provide practical examples, include tables, and answer frequently asked questions to help you make informed decisions.

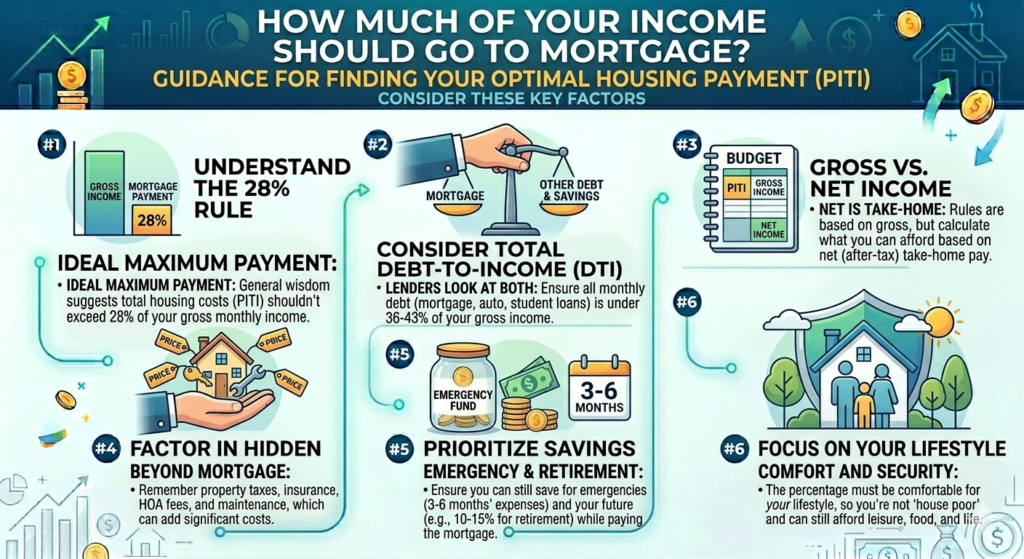

Understanding Mortgage Affordability

The first step in determining how much of your income should go to mortgage is understanding what your mortgage includes. Your monthly mortgage payment usually covers:

- Principal: The amount borrowed from the lender to purchase your home.

- Interest: The cost of borrowing, which depends on your mortgage rate.

- Taxes: Property taxes assessed by your local government.

- Insurance: Homeowners insurance to protect your property.

This total monthly cost is often referred to as PITI (Principal, Interest, Taxes, Insurance). For an accurate assessment, you must consider all four components rather than just principal and interest.

Standard Guidelines for Mortgage Payments

Financial experts often suggest several rules of thumb for determining how much of your income should go to mortgage:

| Guideline | Description | Recommended Percentage of Gross Income |

|---|---|---|

| 28% Rule | Traditional advice: monthly mortgage payment should not exceed 28% of gross income | 28% |

| 36% Rule | Total debt payments, including mortgage, car loans, and student loans, should not exceed 36% of gross income | 36% |

| 30% Rule | Conservative approach for all housing costs including taxes and insurance | 30% |

These benchmarks are intended to balance affordability with lifestyle flexibility, allowing homeowners to maintain savings, retirement contributions, and discretionary spending.

Factors Influencing How Much of Your Income Should Go to Mortgage

Several personal and market factors impact how much of your income should go to mortgage:

- Income Level: Higher income allows a slightly higher allocation without financial strain.

- Existing Debt: A higher debt-to-income ratio reduces the percentage of income that should be allocated to a mortgage.

- Down Payment Size: Larger down payments reduce principal and monthly mortgage payments.

- Interest Rates: Rising rates increase monthly payments, reducing the feasible percentage of income for a mortgage.

- Property Taxes and Insurance: Regional variations can significantly affect monthly housing costs.

- Lifestyle and Emergency Savings: A sustainable mortgage payment allows room for savings, investments, and discretionary spending.

Calculating Your Ideal Mortgage Payment

To calculate how much of your income should go to mortgage, follow these steps:

- Determine your gross monthly income.

- Apply the desired percentage rule (e.g., 28%).

- Factor in property taxes, insurance, and any HOA fees.

- Adjust based on other debt obligations.

Example:

| Annual Salary | 28% of Gross Monthly Income | Estimated PITI | Affordable Home Price |

|---|---|---|---|

| $60,000 | $1,400 | $1,450 | ~$300,000 |

| $80,000 | $1,867 | $2,000 | ~$400,000 |

| $100,000 | $2,333 | $2,500 | ~$500,000 |

Assumes 30-year mortgage at 6% interest with 20% down payment.

Impact of Down Payment on Mortgage Allocation

A larger down payment can reduce how much of your income should go to mortgage, as it lowers the loan principal.

| Home Price | Down Payment | Loan Amount | Monthly Payment (P&I) |

|---|---|---|---|

| $400,000 | 10% ($40,000) | $360,000 | $2,160 |

| $400,000 | 20% ($80,000) | $320,000 | $1,920 |

| $400,000 | 30% ($120,000) | $280,000 | $1,680 |

Higher down payments allow you to allocate a smaller percentage of your income to your mortgage while maintaining affordability.

Budgeting Tips for Sustainable Mortgage Payments

To ensure your mortgage remains manageable, consider these strategies for how much of your income should go to mortgage:

- Conservative Allocation: Keep mortgage ≤25% of gross income for flexibility.

- Balanced Approach: Use the 28–30% rule for conventional affordability.

- Aggressive Strategy: Stretch to 33–35% only if debt is low and savings are strong.

- Emergency Fund: Maintain 3–6 months of living expenses in savings before taking on a mortgage.

- Refinancing: Consider refinancing if interest rates drop, lowering the percentage of income spent.

Examples Across Different Income Levels

Scenario 1: Entry-Level Income ($50,000/year)

| Rule | Monthly Mortgage Payment | Home Price Estimate |

|---|---|---|

| 28% Rule | $1,167 | ~$200,000 |

| 30% Rule | $1,250 | ~$210,000 |

Scenario 2: Mid-Level Income ($100,000/year)

| Rule | Monthly Mortgage Payment | Home Price Estimate |

|---|---|---|

| 28% Rule | $2,333 | ~$450,000 |

| 30% Rule | $2,500 | ~$480,000 |

Scenario 3: High-Level Income ($200,000/year)

| Rule | Monthly Mortgage Payment | Home Price Estimate |

|---|---|---|

| 28% Rule | $4,667 | ~$900,000 |

| 30% Rule | $5,000 | ~$950,000 |

These examples highlight how how much of your income should go to mortgage scales with income while keeping monthly payments sustainable.

FAQs on How Much of Your Income Should Go to Mortgage

Q1: Can I spend more than 30% of my income on a mortgage?

A1: It’s possible, but it may limit savings, retirement contributions, and emergency funds.

Q2: Should I include taxes and insurance in this calculation?

A2: Yes, PITI (principal, interest, taxes, insurance) gives a more accurate view of your total mortgage burden.

Q3: How does my debt-to-income ratio affect mortgage allocation?

A3: Higher debt means you should allocate a smaller percentage of income to your mortgage.

Q4: Is 28% too conservative for high-income earners?

A4: High-income households may stretch to 30–33% if they have low debt and strong savings.

Q5: How do down payments influence this percentage?

A5: Larger down payments lower monthly payments, reducing the percentage of income needed.

Q6: Should I consider an adjustable-rate mortgage?

A6: ARMs may lower initial payments, but they carry the risk of rate increases over time.

Q7: How do property taxes impact affordability?

A7: High property taxes increase PITI, raising the percentage of income allocated to mortgage payments.

Conclusion

Determining how much of your income should go to mortgage is crucial for responsible homeownership. Using rules of thumb like 28%–30% of gross income, considering down payments, factoring in taxes and insurance, and maintaining emergency savings ensures your mortgage is sustainable.

By carefully calculating monthly payments and evaluating personal finances, you can confidently choose a mortgage that supports your lifestyle, long-term financial goals, and overall financial health. Whether you’re a first-time buyer or planning your next home purchase, knowing how much of your income to allocate helps you avoid financial strain and enjoy homeownership with peace of mind.